April 2026 Market Update: Single-Family Homes in the South Island

COWICHAN VALLEY

Summary: As of April 2026, the average sale price for single-family homes was $856,816, with a sell-to-list ratio of 44.85%.

Sales Activity: A total of 75 single-family homes were sold in the Cowichan Valley during April 2026, marking a decrease from homes sold in April 2025 and a marked increase from 54 homes in March 2026.

Listings & Inventory: The market saw 171 new single-family home listings in April 2026, up 25.7% compared to 136 listings in April of last year. As of the end of April 2026, 323 homes were actively listed, up from 307 homes available at the same time last year.

Pricing Trends:

• The average sale price in April 2026 was $856,816, reflecting an increase from April 2025’s average of $833,023.

• Compared to March 2026’s average of $861,998, prices have strengthened slightly.

• For the 12-month period ending in April 2026, the median sale price stood at $785,500.

Annual Performance: Over the past 12 months, 658 single-family homes were sold, which represents an approximately 6.5% decline compared to the 704 sales in the same period ending in April 2025. Despite the slower pace of sales, the average selling price for the year is up by 4.03%.

Market Supply & Days on Market:

• The supply of homes increased to 4.3 months in April 2026, down from 4.9 months in April 2025.

• Homes sold in April 2026 took an average of 41 days to sell, compared to 32 days in April last year.

This summary highlights the key market trends and performance for single-family homes in the Cowichan Valley, helping homeowners and buyers stay informed about the latest developments. Feel free to reach out for further details or if you need personalized advice!

Condo & Townhome Market Update

Condominiums

In April, the condominium market saw 8 units sold, up from 5 in March 2026. Sales are up from the 5 units sold in April of last year. The average price for condo apartments over the past 12 months ending in April 2026 fell to $340,366 - a 4.11% decrease from last year's average of $354,947.

Townhomes

The townhome market experienced a jump, with 14 sales in April, an increase from both the 13 units sold in March 2026 and 9 in April 2025 (a 55.6% year-over-year increase). The average price for townhomes over the past 12 months ending in April reached $567,097, up 0.96% from $561,685 during the same period last year.

VICTORIA

Summary: In April 2026, the benchmark price for single-family homes in the Victoria Core reached $1,339,100, reflecting a 1.2% month over month decrease from April 2025.

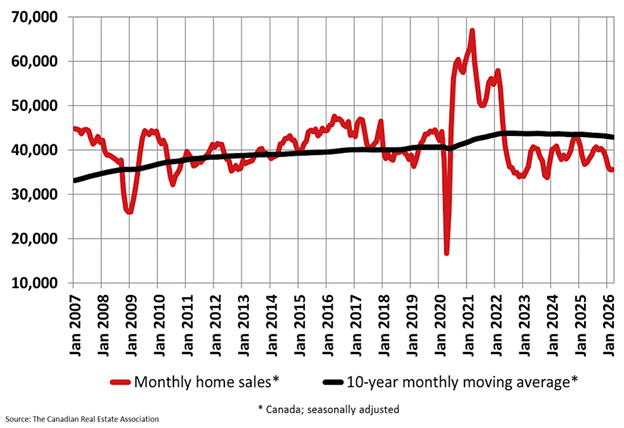

Canadian Home Sales Activity Little Changed in March

Ottawa, ON April 16, 2026 – The number of home sales recorded over Canadian MLS® Systems was virtually unchanged (-0.1%) on a month-over-month basis in March 2026. (Chart A)

“Home sales activity remained at lower levels in March, as rising global economic uncertainty, along with a mid-month jump in fixed mortgage rates tied to incoming higher inflation, piled on to an already shaky economic start to the year,” said Shaun Cathcart, CREA’s Senior Economist. “2026 is still expected to see a modest amount of upward momentum in sales and a stabilization in prices as some pent-up first-time buyer demand enters the market, but the forecast for the year has had to be revised downward. The timing of higher mortgage rates, along with the perception they may be temporary, could keep would-be buyers away at the most active time of year – April, May, and June – as they wait for rates to come back down.”

March Highlights:

• National home sales were almost unchanged (-0.1%) month-over-month.

• Actual (not seasonally adjusted) monthly activity came in 2.3% below March 2025.

• The number of newly listed properties edged down 0.2% on a month-over-month basis.

• The MLS® Home Price Index (HPI) fell 0.4% month-over-month and was down 4.7% on a year-over-year basis.

• The actual (not seasonally adjusted) national average sale price was down 0.8% on a year-over-year basis in March 2026.

• National home sales were almost unchanged (-0.1%) month-over-month.

• Actual (not seasonally adjusted) monthly activity came in 2.3% below March 2025.

• The number of newly listed properties edged down 0.2% on a month-over-month basis.

• The MLS® Home Price Index (HPI) fell 0.4% month-over-month and was down 4.7% on a year-over-year basis.

• The actual (not seasonally adjusted) national average sale price was down 0.8% on a year-over-year basis in March 2026.

Chart A

New listings edged down a slight 0.2% on a month-over-month basis in March 2026. Lower monthly sales numbers so far in 2026 could in part be due to the fact new supply is running at the lowest levels since mid-2024.

With new supply and sales both little changed in March, the national sales-to-new listings ratio remained at 47.8%. The long-term average for the national sales-to-new listings ratio is 54.8%, with readings roughly between 45% and 65% generally consistent with balanced housing market conditions.

“While the interest rate situation has recently changed, what could be a challenge for a buyer looking for a fixed rate mortgage may also be seen as more choice and less competition for those choosing a variable rate,” said Garry Bhaura, CREA’s 2026-2027 Chair. “Spring tends to be a busier time of year for the housing market, even if it may not be quite as busy as we were expecting not so long ago. For those of you not impacted by the recent jump in mortgage rates, get working with a local REALTOR® today.”

There were 167,524 properties listed for sale on all Canadian MLS® Systems at the end of March 2026, up just 1% from a year earlier and 10.6% below the long-term average for that time of the year. Overall supply has generally been declining since May of last year.

There were five months of inventory on a national basis at the end of March 2026, unchanged from January and February and right in line with the long-term average for the measure. Based on one standard deviation above and below that long-term average, a seller’s market would be below 3.6 months, and a buyer’s market would be above 6.4 months.

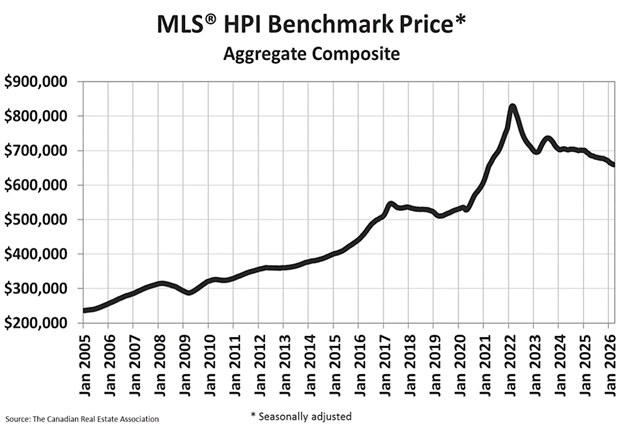

The National Composite MLS® Home Price Index (HPI) edged down 0.4% on a month-over-month basis in March, not a small decline but smaller than in February and just half the decline recorded in January. This aligns with sale-to-list price ratios that have been tightening up in recent months as fewer listings have been coming onto the market. Price stabilization is part of CREA’s forecast for 2026, and will be an important milestone to reach for buyers eventually re-entering the market in larger numbers. The non-seasonally adjusted National Composite MLS® HPI was down 4.7% compared to March 2025, down slightly from the 4.8% year-over-year decline registered in February. (Chart B)

Chart B

Regionally, prices remain down on a year-over-year basis in British Columbia, Alberta, and Ontario, offsetting gains in other provinces.

The non-seasonally adjusted national average home price was $673,084 in March 2026, dipping 0.8% from the same month last year.

The next CREA statistics package will be published on Thursday, May 14, 2026.

Bank of Canada maintains policy rate at 2¼%

FOR IMMEDIATE RELEASE

Media Relations

Ottawa, Ontario

April 29, 2026

The Bank of Canada today held its target for the overnight rate at 2.25%, with the Bank Rate at 2.5% and the deposit rate at 2.20%.

The evolving conflict in the Middle East is causing heightened volatility and US trade policy continues to reshape global trade patterns. Both are ongoing sources of uncertainty. The Bank’s April outlook assumes tariffs remain unchanged and the global benchmark price of oil declines to US$75 per barrel by mid 2027.

The Iran war has led to sharply higher energy prices and transportation disruptions, diminishing growth prospects in oil-importing countries and boosting inflation worldwide. In the United States, growth is still expected to be solid over the projection horizon, boosted by AI-related investment and consumption growth. China’s economy is being supported by robust exports. In the euro area, higher prices for oil and natural gas will weigh on economic activity.

Financial conditions have been volatile, reflecting daily developments in the Middle East and shifting market expectations for inflation and interest rates. Bond yields are modestly higher since January while equity markets, which weakened sharply at the outset of the war, have recovered. Since the start of the war, the US dollar has appreciated against most major currencies. The Canada-US exchange rate has been relatively stable.

Financial conditions have been volatile, reflecting daily developments in the Middle East and shifting market expectations for inflation and interest rates. Bond yields are modestly higher since January while equity markets, which weakened sharply at the outset of the war, have recovered. Since the start of the war, the US dollar has appreciated against most major currencies. The Canada-US exchange rate has been relatively stable.

Overall, the global economy is expected to grow by about 3% in 2026, 2027 and 2028. Projections for inflation over the next year are revised up because of the jump in energy prices.

The outlook for economic growth in Canada is little changed from the January Monetary Policy Report (MPR) projection. After a contraction in the fourth quarter of 2025, growth is forecast to have resumed in early 2026. Consumer and government spending are supporting economic activity, while tariffs and trade uncertainty are weighing on exports and business investment. Housing activity declined in the fourth quarter and is being held back by slow population growth, economic uncertainty and ongoing affordability issues. The labour market is soft, with subdued employment growth over the past year and job losses in sectors targeted by US tariffs. The unemployment rate remains in the 6½% 7% range, reflecting both weak hiring and fewer job seekers.

The Bank’s April forecast projects GDP growth of 1.2% in 2026, rising to 1.6% in 2027 and 1.7% in 2028 as growth in exports and business investment resumes along a lower trajectory. With GDP growing slightly above potential, the current excess supply in the economy is gradually absorbed. While the war in Iran may alter its composition, overall GDP growth is little changed in the updated forecast: Since Canada is a large net exporter of oil, higher oil prices increase national income even as consumers are squeezed by higher gasoline prices.

CPI inflation climbed to 2.4% in March because of sharply higher gasoline prices. The March increase follows several months of slowing inflation data. Core inflation has been easing and held steady at just above 2% in the most recent inflation report. The proportion of components of the CPI basket rising above 3% has also declined in recent months. As expected, so far there is little evidence that oil prices have fed through more broadly to goods and services prices, but this warrants close attention in the months ahead. Near-term inflation expectations have moved up with higher gasoline prices and still-elevated food price inflation, but longer-term inflation expectations have remained anchored.

CPI inflation will likely rise further in April to about 3%. Based on the assumption that oil prices will ease, inflation is forecast to come down to the 2% target early next year and remain around 2% over the projection horizon.

Against this backdrop and taking into account the current projection, Governing Council decided to maintain the policy rate at 2.25%. We are closely monitoring the impact of the conflict in the Middle East and how the economy is responding to US tariffs and trade policy uncertainty. Governing Council is looking through the war’s immediate impact on inflation but will not let higher energy prices become persistent inflation. As the outlook evolves, we stand ready to respond as needed. The Bank is committed to maintaining Canadians’ confidence in price stability through this period of global upheaval.

Information note

The next scheduled date for announcing the overnight rate target is June 10, 2026. The Bank’s next MPR will be released on July 15, 2026.

The next scheduled date for announcing the overnight rate target is June 10, 2026. The Bank’s next MPR will be released on July 15, 2026.